Meituan Stock (3690.HK) Analysis: Why I Still Own Them even in this “Delivery-war” Era

Disclosure: I’m biased. I own both Meituan (HK:3690) and Alibaba (HK:9988).

Alibaba is ~30% of my portfolio. Meituan is ~6%. I’m writing this to explain how I think about the business, the current price war, and what I track over a 3–5 year horizon. This is not financial advice.

Why I changed my mind on food delivery

For years I stayed away from food delivery platforms. Switching felt too easy. Price wars felt endless. The numbers looked like a treadmill. That changed after using Meituan on a trip to China in 2024. ETAs were reliable, coverage felt dense, service recovery was quick, and Dianping’s reviews actually influenced what I picked. I could get dinner, pain relief tablets, a last-minute massage slot, and a grocery top-up inside one app. It felt like “life in 30 minutes,” not just another takeout button.

That experience sent me back to first principles: What makes Meituan different, what has changed in 2025, and how should a retail investor judge the next few quarters without getting lost in headlines?

What Meituan actually is (for normal people)

Meituan is a local-services super app. The core is on-demand food delivery. Around that core are in-store services, trusted discovery and reviews through Dianping, local travel and tickets, instant retail and groceries, plus a long tail of convenience features. The app connects hundreds of millions of users to millions of nearby merchants, then coordinates a very large rider network to move things quickly.

The value is not just the order. It is density, dependable ETAs, discovery that converts, and the ability to monetize high-intent searches with ads and sponsored placement. Meituan’s own filings split revenue into delivery services, commissions, online marketing services, and “other.” Ads and placement inside Meituan/Dianping are the quiet, higher-margin engine when conditions are normal.

Think about three buckets;

- Commissions (take rate). Every completed order throws off a small fee. This scales with order growth and category mix.

- Online marketing and ads. This is where margin hides. When a hungry user searches “noodles within 2 km in 30 minutes,” the click is close to a sale. Merchants pay for ranking and performance ads because returns are measurable. When ad ROI holds up, this line grows faster than orders.

- Other services. Instant retail, groceries, bikes, power banks, local-life add-ons. Useful for engagement and share of wallet, sometimes heavier on ops in the early phase.

Delivery fees surge through the system and look big, but they are lower margin and mostly about keeping the flywheel spinning: fast, predictable delivery keeps users and merchants loyal. Over time, margin expansion depends far more on ad yield and operational density than on absolute delivery fees.

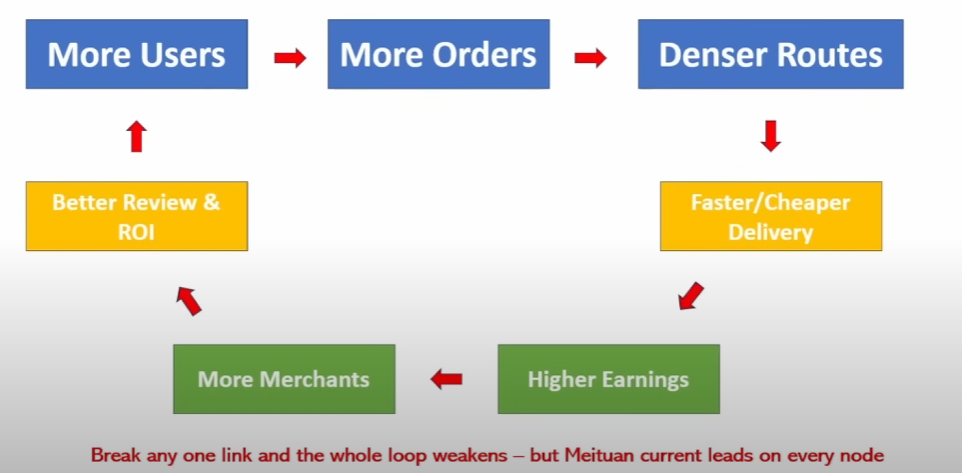

Meituan’s moat is a network that is hard to copy city by city.

• Users ↔ Merchants ↔ Riders. More users bring more orders. More orders raise route density. Higher density improves rider earnings per hour and lowers cost per drop. That produces faster ETAs, which lifts conversion and keeps ad ROI healthy.

• Dianping trust. A credible review layer drives discovery and conversion. That makes paid placement more targeted and stickier.

• Soft lock-ins. Membership deals, coupons, merchant tools, POS, working capital and analytics keep both sides engaged. Once a merchant’s day-to-day is wired into Meituan’s tools, switching is not free even if downloading a rival app is.

This is not magic. It is urban plumbing. Anyone can subsidize orders. Not many can deliver dense, repeatable execution across hundreds of cities, while monetizing intent through ads at scale. Meituan has been built for that.

What changed in 2025: a real subsidy war

2025 brought a genuine price war in instant retail and food delivery. JD tried to leverage its logistics strength to enter the space. Alibaba pushed “instant commerce” inside Taobao and integrated Ele.me to speed up last-mile delivery. Within a month of launch, Alibaba said its Instant Commerce portal crossed 40 million daily orders, which shows how quickly Taobao can redirect traffic. The near-term question is not who can yell the biggest peak, but who can keep share once subsidies cool and ad ROI has to stand on its own.

In Q2, Meituan’s adjusted profit fell sharply as subsidy pressure rose and “instant retail” competition intensified. JD’s profit roughly halved as its push into local delivery weighed on earnings. Alibaba has the broadest base and can cross-promote inside Taobao, but even for them heavy promotions dent cash generation when they lean in.

Mainland analysts describe a battle-loss ratio: how much operating profit each side sacrifices for every unit of market share gained or defended.

Here’s how it works; If Platform A burns 10 and rivals together burn 28 to move the market a similar amount, A’s defence is more efficient. The headlines will still look ugly, but attrition favours the player with denser operations and better ad yield per order. The ratio can shift quarter to quarter, so the real test is over a few quarters, not a single spike. And yes, Meituan is currently the one burning 10, whilst JD.com and Alibaba is the other 28, and still not taking away significant market share from Meituan.

My read today: the winner of this phase is not “who shouts the largest daily orders,” it is “who defends share at the lowest burn per incremental order and emerges with ad budgets intact.”

The competition headline in this Food Delivery War

Alibaba (Taobao + Ele.me + Amap/AutoNavi). The Instant Commerce tab pipes Taobao’s huge traffic into one-hour delivery using Ele.me’s last-mile network. On top of that, Amap (Gaode)—Alibaba’s maps app—has moved directly into Dianping’s turf with “Street Stars,” an AI-driven ranking layer for restaurants, hotels and attractions.

Amap’s baseline DAU is ~170 million, and it just hit a record 360 million DAU on Golden Week, helped by ¥1B in coupons and in-store/ride-hailing subsidies. In raw reach, that easily puts Amap ahead of Dianping on “people seeing lists,” which is why merchants are paying attention. The open question is trust and staying power: can Amap’s rankings become the default place people believe and use to decide where to eat and what to book—without heavy subsidies—and will that traffic actually push sales for merchants the way Dianping does today?

Until we see sustained merchant ROI and repeat usage after promos cool, Meituan still has the stronger review-to-conversion funnel, even if Amap’s top-of-funnel scale is larger right now. The critical investor question remains efficiency after the hype: can Alibaba’s new stack match Meituan on ad yield per user and average delivery cost per order once promotions normalize.

JD. Logistics excellence does not automatically win same-hour local delivery. After an initial surge, JD’s earnings came under pressure and management has moderated its push in phases. If JD stays cautious, the battleground defaults to Meituan vs Alibaba, which is the scenario I underwrite.

Douyin local-life. Douyin is a monster at discovery and conversion in short video. It will pull some merchant marketing budgets, but it is not built to own last-mile everywhere. Expect Douyin to be a strong acquisition channel and a pressure point on ad pricing, not a replacement for dense same-city logistics in the near term.

What drives unit economics

Two words: order density.

• Higher density raises rider trips per hour, which increases rider earnings and reduces cost per drop.

• Shorter routes improve ETAs, which boosts conversion and makes ad spend more predictable for merchants.

• Predictable returns bring merchants back to the ad platform, which is the quiet margin engine.

When the environment is normal, Meituan’s disclosures highlight online marketing as a key driver. During a price war, that engine can slow, but it is also what powers margin recovery later, once promos fade. Keep an eye on how that line behaves after the current subsidy peak.

My KPI box for the next four quarters

• Order growth and order density. Volume tells you demand. Density tells you whether unit costs will actually fall.

• Take rate and ad revenue mix. If the ad mix recovers, the machine is healing.

• Delivery cost per order and ETA reliability. Reveals whether subsidies are masking weak execution.

• Merchant engagement. Returning ad buyers with higher spend per merchant is the best leading indicator.

A short word on overseas bets.

Meituan is testing the playbook outside the mainland. Success means a local partner mesh, disciplined city selection, and clear payback windows. Failure looks like creeping opex without density. I treat KeeTa and other tests as a watchlist item, not a pillar. If these become material, I will update the weight in the thesis.

Is Meituan (HK:3690) still undervalued today?

During a heavy promotion phase, earnings can swing negative even if the engine is intact. I avoid false precision and use simple cross-checks:

• Forward P/E once earnings normalize.

• Price to gross profit versus a realistic growth band.

Recent coverage and company commentary make it clear that competition in instant retail is squeezing near-term profitability, while revenue still grows. The path back to better multiples is not mysterious. It needs steady orders, a stable or rising ad mix, and delivery costs trending down as density comes back.

I own both Meituan and Alibaba because I want the category’s long-run growth, not just a single quarterly winner.

My base case is a two-player market with acceptable unit economics once subsidies cool. If forced to write it down, I expect something like a 60/40 split in Meituan’s favour over time. I expect ugly prints in subsidy-heavy quarters. My holding period is at least 3–5 years.

What would change my mind?

Three things, together, for multiple quarters:

- Ad mix deteriorates even after promotions cool, which means high-intent monetization is weakening.

- Unit cost rises and ETAs slip despite volume recovering, which means the density engine is breaking. (which might also mean Meituan is losing its efficiency/execution premium)

- Merchant budgets shift away from Meituan to rivals permanently, which means ad ROI is not competitive.

If these show up together, the flywheel is stalling, and I would reduce.

If you would like to see my trailing 5-year investment track record, you can head here.