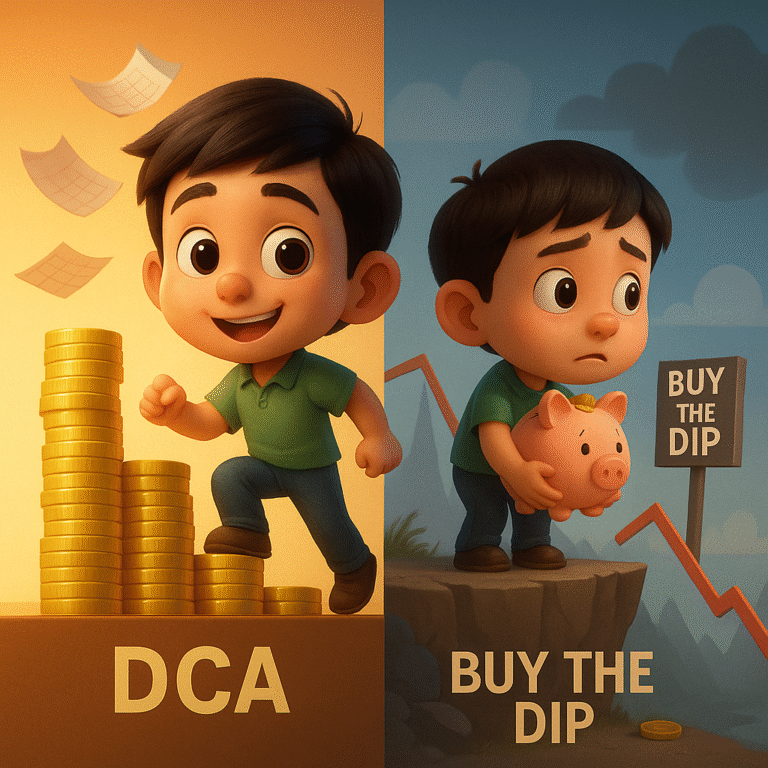

Buy the dip vs. Dollar cost averaging: You’ll be surprised

Most investors have heard “time in the market beats timing the market.” It sounds like a slogan. Nick Maggiulli stress-tested it in a way that matters for people who try to hoard cash and “buy the dip.” His result is uncomfortable for dip hunters:

- A perfect, all-knowing buy-the-dip strategy underperforms dollar-cost averaging in over 70% of rolling 40-year windows from 1920–1979.

- Miss the exact bottom by just two months and it underperforms DCA 97% of the time.

Maggiulli sets up two strategies that invest for 40 years.

- DCA: invest a fixed amount every month.

- Buy the dip: save cash every month and purchase only at the absolute bottom between any two all-time highs. In the base test, you know those bottoms with perfect hindsight. No trading in or out once you buy.

Despite perfect knowledge, buy-the-dip lagged DCA more than 70% of the time. The reason is not magic. It is time. While the dip buyer sits in cash waiting for a sale, the DCA buyer quietly compounds. And in a market with a positive long-run drift, months lost to waiting are hard to make back.

Provider research points in the same direction. Schwab finds the cost of waiting for perfect timing typically exceeds the benefit even if you could time well. Their practical guidance is to get invested sooner and stick to a plan. Morningstar has run similar tests that show staying invested beats common timing schemes across regimes.

Why trying to ‘time the bottom’ loses

- Cash drag: While you wait, cash usually trails equities by a wide margin over long horizons. The gap compounds against you.

- Rebounds are fast: A large share of the market’s best days cluster during bear markets or right after the bottom, when timing still feels scary. Miss those days and long-term results suffer. Hartford’s lookback shows roughly 42% of the S&P 500’s strongest days in the last 20 years happened during bear markets and another 36% in the first two months of a new bull.

- Big dips are rarer than memory suggests: Corrections happen, but deep bear-market bottoms that justify a long wait are infrequent. Recent rundowns from Reuters and others show 10% corrections are common, yet only a subset become 20% bear markets, and many resolve faster than expected.

Where did ‘buy-the-dip’ excel?

There are windows where buying a huge early crash helped.

- 1929–1932 inside a 1928–1957 start: The strategy bought the 1932 bottom early. A $100 purchase at that trough compounded to multiples in real terms by the end of the window. DCA still worked, but the single early crash gave the dip strategy a tailwind.

- 1995–2018 with March 2009: Buying the 2009 low produced a visible bump, although the outperformance relies heavily on that one entry. Miss it by two months and the edge disappears in the aggregate tests.

These are the exceptions that prove the rule. They require a large, early crash and near-perfect execution.

Where did ‘buy-the-dip’ struggle

- • 1975–2014 starts: The big bear ended in 1974. Starting in 1975 meant you waited years for a new all-time high and then even longer for a meaningful “between ATHs” dip. With no big early crash to buy, the strategy sat in cash while DCA kept compounding. Result: buy-the-dip lagged by a lot.

- • Long, grinding bull markets with brief pullbacks: Many declines between ATHs are shallow and short. You either never get your perfect trigger or you get it late. The cost of waiting dominates.

Reality Check for ‘buy-the-dip’ objections

“But I can earn yield on cash while I wait.” True, but over full cycles the equity premium tends to dominate. Schwab’s work on the cost of waiting and cash’s historical underperformance relative to stocks explains why the drag remains.

“I don’t need to nail the bottom, just get close.” The test already tried “close.” Two months late took the win rate from 30% to 3%. That is the whole problem. Close still loses most of the time.

“Timing worked in [insert crash].” Sometimes. The question is repeatability over many starting points. Morningstar’s repeated head-to-heads show timing loses to staying invested far more often than people expect.

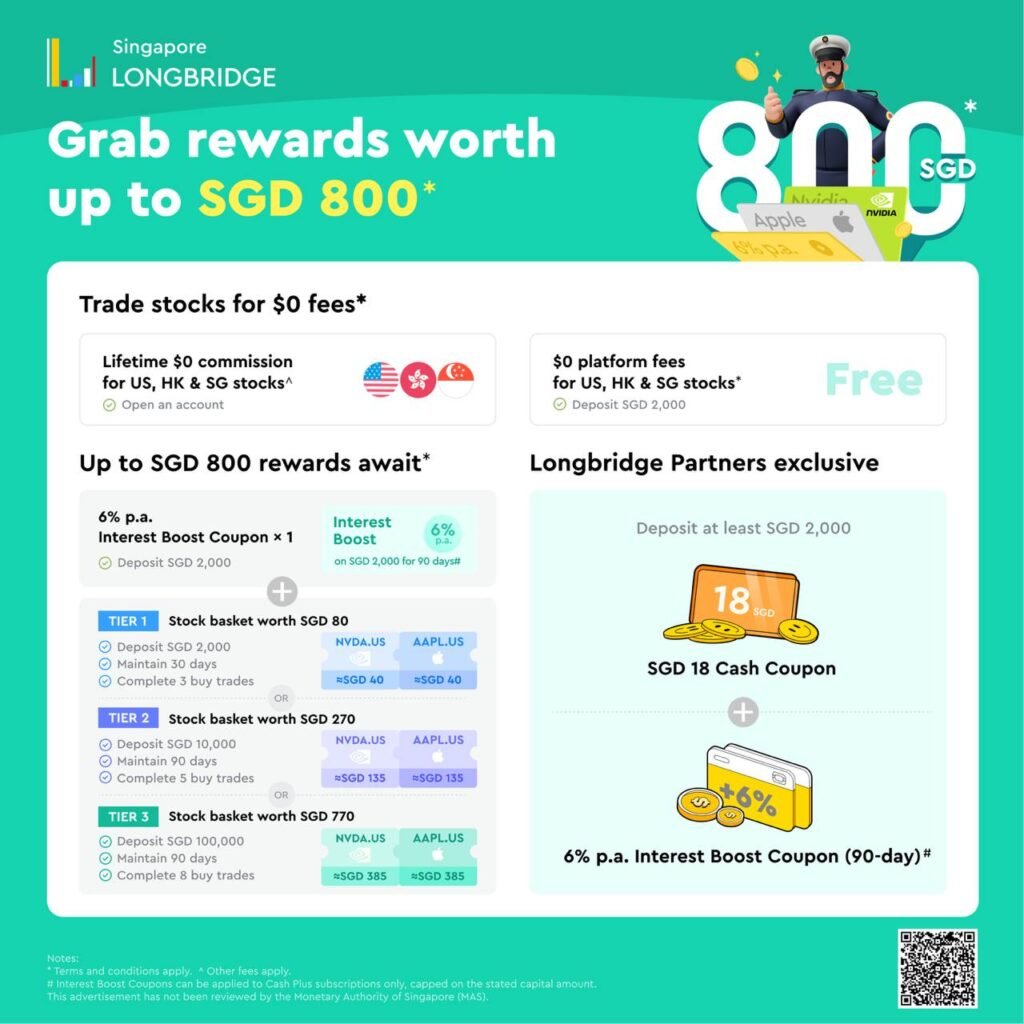

If you’re ready to take advantage of the power of dollar-cost-averaging today, you can sign up for a brokerage account with LongBridge (a trusted broker that we use ourselves), and take advantage of their new user sign-up promotion worth up to S$800 today!

Frequently Asked Questions

Is buying the dip better than DCA for beginners?

Usually no. DCA keeps your money working and removes guesswork. Dip buying can help a little if it is a small, optional top-up. It should not replace your base plan.

How often do big dips actually happen?

True “everything is on sale” moments are rarer than you think. You might wait years. That is a long time to leave money idle.

Does DCA still work in a bear market?

Yes. You buy more shares when prices are lower without having to predict bottoms. When the market recovers, those extra shares help.

Should I pause DCA to save for the “next” dip?

Pausing is usually harmful. You give up compounding time. If you want cash for dips, decide on a small, fixed cash buffer and keep DCA running in the background.

Can I mix DCA with buying the dip without guessing bottoms?

Yes. Keep your regular DCA. If the market falls by a level you can tolerate emotionally, add a small top-up that you can afford. If you are not sure, skip it. The base plan is doing most of the work.