There are two performance numbers investors keep running into. One is the time weighted return, often written as TWRR. The other is the money weighted return, usually shown as MWRR or XIRR. Both sound technical. Both appear in portfolio reports, factsheets, and finance blogs. The problem is that most explanations are written for exams rather than for real investors who are trying to grow family wealth.

Here is the simple version. Time weighted return shows how the investment itself performed. Money weighted return shows how you performed with your timing and cash flows. If you run your own money at home, both numbers matter, but for day-to-day decision making, the money-weighted return is often the better mirror.

I will keep this practical and personal. I have tracked my portfolio for almost five years, and these were my results against a like-for-like S&P 500 benchmark using Portseido.

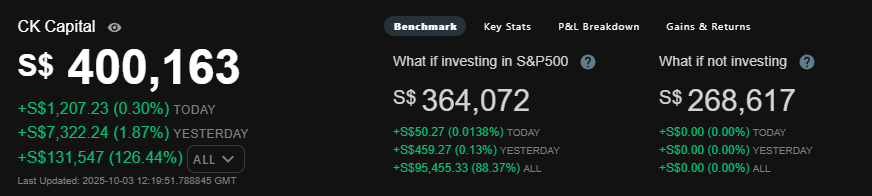

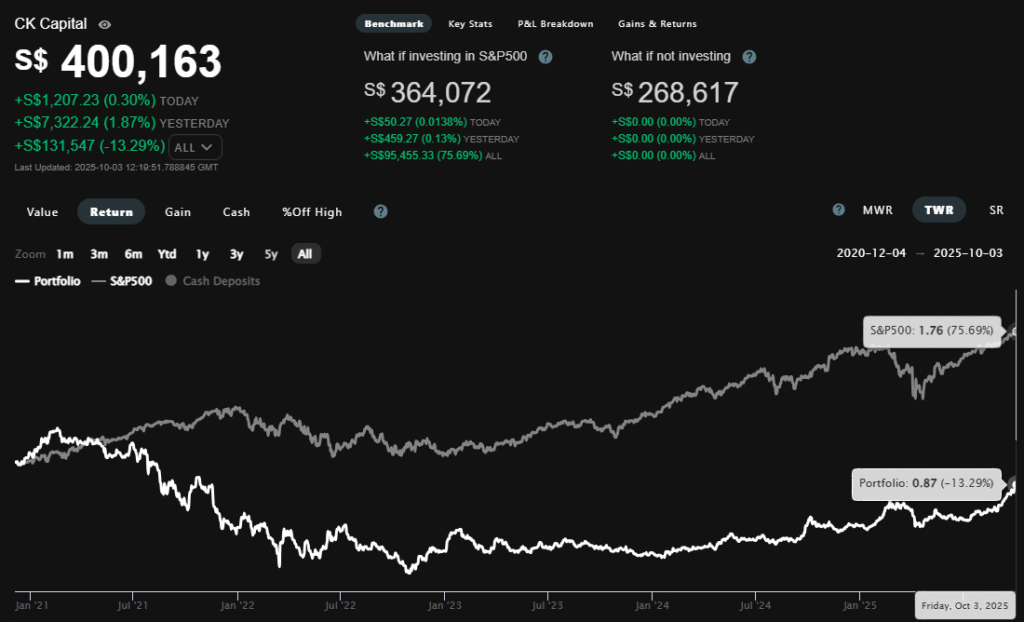

As of the time of this writing, my money weighted return shows about +126% returns.

In dollar terms, I have roughly $131,000 SGD of gains on about S$268K contribution. During the same period, my time weighted return shows about (NEGATIVE) -13% performance. Same portfolio, same dates, two different stories. Understanding why they disagree will help you measure progress and improve your process.

I’ll share with you why later.

What each measure actually tells you

Time weighted return removes the effect of your deposits and withdrawals and focuses only on how the investment grew from period to period. Fund managers prefer it because they cannot control when investors add or redeem. TWRR is a clean way to compare the strategy behind a unit trust, mutual fund, or ETF. If you are judging a manager’s skill or comparing two funds over the same dates, time weighted makes sense.

Money weighted return includes the size and timing of your cash flows. It is the internal rate of return of your personal journey. If you add more capital after a selloff, or if you add at peaks and then the market pulls back, your money weighted return will move accordingly. If your goal is to track how your savings plan, contributions, and rebalancing affect your net worth, MWRR is the number to watch.

An example that shows the gap

Imagine a fund that doubles in Year 1 and then halves in Year 2.

Year 1: +100%

Year 2: -50%

TWRR over two years = (1+1) × (1-0.5) – 1 = 0%. The strategy “did” 0% total.

Now two investors make different choices:

Investor A puts $10,000 at the start and never adds more. Ending value after two years is still about $10,000. Their MWRR is about 0%.

Investor B waits, sees the big gain, then puts $10,000 at the end of Year 1. They ride the -50% drop and end around $5,000. Their MWRR is about -50%.

Same fund. Same TWRR. Very different investor experiences.

So What Happened to my Portfolio?

I started with a tiny account and a very concentrated bet in Chinese tech. That position fell almost 70 percent from my entry, which dragged the early periods of my track record down. Time weighted return stitches every period together as if no money went in or out, so those early drawdowns keep pulling the average lower even after things improved. On that basis, my portfolio still shows about negative 13 percent since inception.

My actual journey was different. Over the next four years I kept adding capital, broadened the portfolio, and bought more at lower prices. Money weighted return cares about when the dollars arrived and how long they worked. Because most of my contributions happened during the big decline, it took advantage of the lower prices. That is why my money weighted return sits around plus 126 percent and why I have roughly S$131,000 in gains on about S$268,000 contributed, even though the time weighted number is negative.

In my case the time weighted number is still negative because it chains each return period as if no cash moved in or out. Early drawdowns dominate that chain. The money weighted number is positive because the actual dollars I added over time were invested at more attractive prices, and later gains compounded on a larger base. Neither number is wrong. Each one is answering a different question.

Track what really matters.

I use Portseido to see my money weighted returns and a like-for-like benchmark based on my actual investment dates. If you want transparent, no-nonsense performance tracking, start the 14-day free trial.

What to do with TWRR vs. MWRR?

If you are selecting funds or comparing ETFs, rely more on time weighted return. You want to compare strategies on equal footing across the same dates. Pair it with simple checks on fees, tracking difference, and risk.

If you are managing your own savings plan, rely more on money weighted return. You want to know whether your actual cash flows, position sizes, and rebalancing rules are growing family wealth. Compare your XIRR to a like-for-like benchmark that is funded on your actual dates. Most investors never do this and it is the cleanest way to see whether your process adds value beyond a low-cost index.

If you are serious about improving results, track both. Time weighted will keep you honest about the quality of the ideas and the underlying strategy. Money weighted will keep you honest about behavior, timing, and discipline.

A short word on ‘comparing’ CAGR

CAGR is the compound annual growth rate between a starting value and an ending value. It removes the noise of the path and shows the smooth rate that would have produced the same ending wealth. It is useful for quick comparisons, but it hides the role of cash flows and volatility. For a household investor, the levers that matter are savings rate, time in market, and process quality. CAGR is the outcome of those inputs. Do not chase a target CAGR without first fixing the inputs you control.

In Summary, When Comparing..

Which is more important, time weighted or money weighted return? If you are evaluating a fund, time weighted return is the right lens. If you are evaluating your own progress, money weighted return is the right lens. The most useful practice is to look at both, understand what each is saying, and then make a small process improvement you can keep for the next decade. That is how wealth compounds in real life.

My summary in one line: Time weighted shows how the investment did. Money weighted shows how you did.

FAQ

What is time weighted return in plain English?

It is a measure of portfolio performance that strips out the effect of your deposits and withdrawals. It is best for comparing strategies and managers across the same time periods.

What is money weighted return or XIRR?

It is the internal rate of return of your actual cash flows and balances. It includes timing and size of contributions and withdrawals, so it reflects your real experience.

Which should I use to track my portfolio performance?

Use XIRR to measure your personal results. Use time weighted return to benchmark your strategy selection.

How do I calculate XIRR quickly?

List every cash flow with dates in a spreadsheet. Contributions are negative, withdrawals are positive. Add the current portfolio value as a final positive number. Use the XIRR function to get your personal annualized return.

Why does my return not match my fund’s factsheet?

The factsheet reports time weighted returns. Your app likely shows money weighted returns. Different questions, different answers.